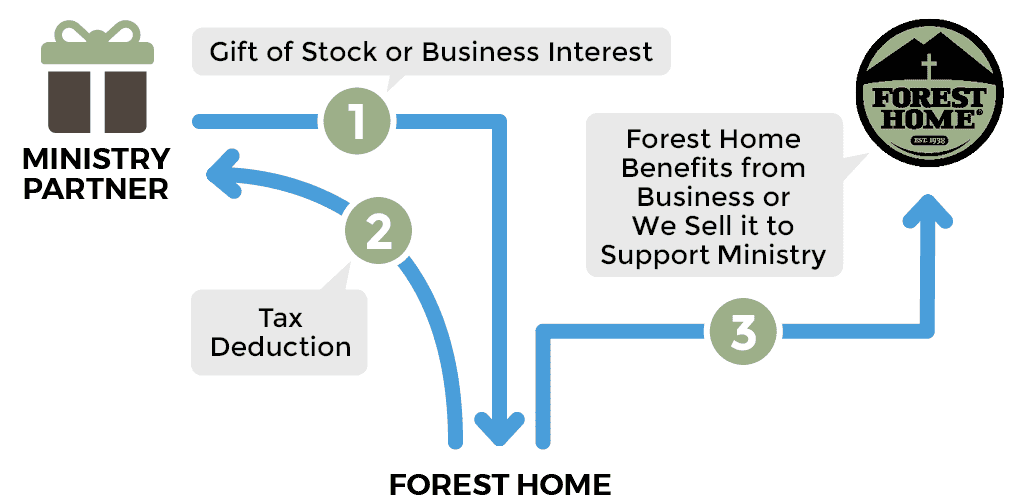

As an entrepreneur, you can grow your business and also accomplish your ministry goals. Gifts of business interests, like stock in a closely held corporation or shares in an investment partnership, can provide you with tax and income benefits and further the ministry of Forest Home.